In investing, there is an age old way of dividing up the market into two types of companies - growth companies and value companies. The distinction is based on a basic metric, price-to-earnings or P/E Ratio.

For companies with a higher P/E Ratio, it means the market is expecting them to grow in order to justify those valuations. And those with lower P/E Ratios means they are a relative value and therefore do not need to grow as much to justify their valuations.

There are two key things I find flawed about this oversimplified way of dividing up the market.

- The P/E metric has nothing to do with growth. What makes an investment worthwhile is whether revenue and income are growing. This metric does not measure that at all. A company could be growing revenue but losing more money as they grow. Or they may not be growing at all but still sport a high PE Ratio for some unjustified reason.

- The P/E metric only looks at one component of value but not the whole picture. P/E only looks at earnings to equity (Net Income per share) compared to the stock price. It is missing the entire debt piece. There might be a company that has a low P/E ratio but a ton of debt that could never be serviced. This means it is on its way to bankruptcy (meaning the stock becomes worthless), but would still be considered a great value.

Growth and value are not opposite sides of a coin, they actually are completely unrelated. Yes in theory higher growth companies will have a higher valuation but that is not always the case. Same thing goes that if a company is not growing, it may still be wildly overvalued.

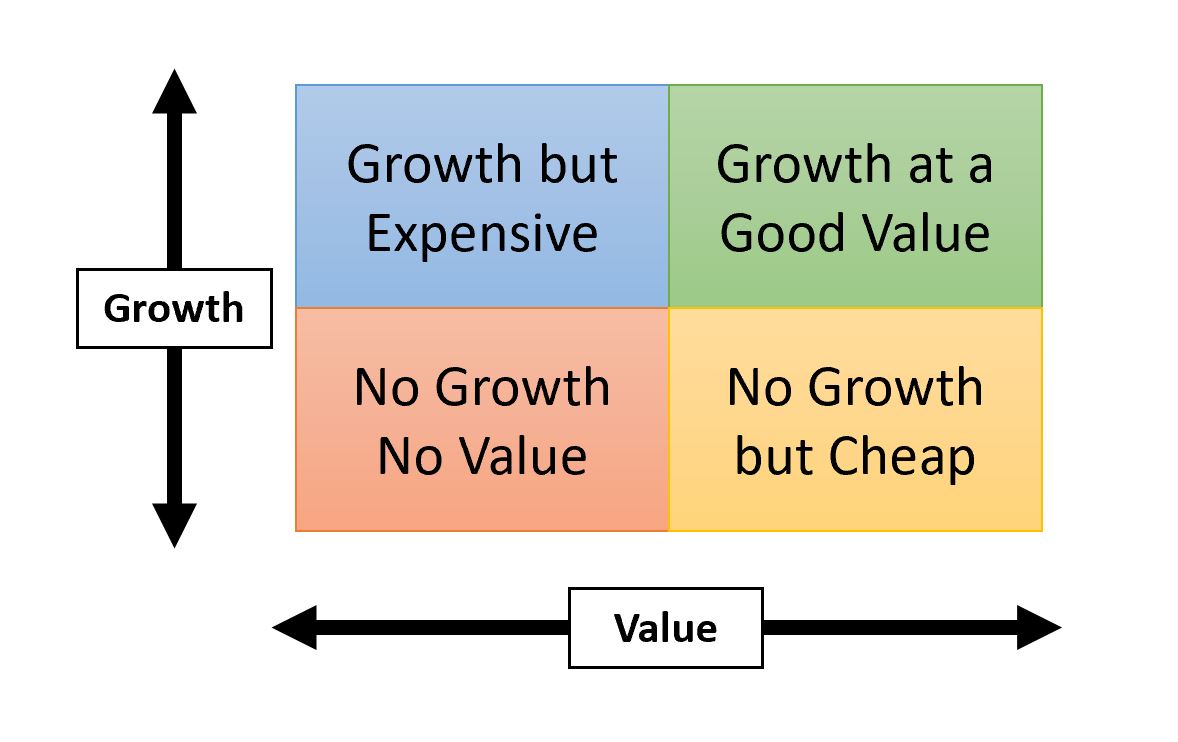

When I think about stocks, I think in a 4-square grid format. On one axis is whether the company is actually growing revenue and income. On the other axis is looking at the value of the company as a whole by taking its equity market capitalization and adding its debt and subtracting its cash (this is called Enterprise Value).

This then puts companies into four categories:

- Not growing and not a good value. Obviously try to avoid these.

- A good value but not growing. Historically companies like this have performed well but the last 10 years have been difficult for these types of companies.

- Growing but not a good value. This category has performed the best over the last 10 years. Many technology companies that have risen so much have indeed been able to grow into their valuations from years' past.

- Growing and a good value. This is the holy grail in my opinion. These are the least risky investments because they are already a great investment and as they grow they become an even greater investment.

Comments

Post a Comment